Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Compound Effect: Building Your Household’s Wealth

Wealth is within reach for many people; however, the majority of Americans say it’s not likely they’ll become rich.1 While younger people are more likely to say they’ll achieve wealth one day, only 34 percent of people aged 30 to 49 and 21 percent of people aged 50 or older say the same. There is no secret to becoming rich: it takes time, sacrifice and good financial sense. Here are a few ways to build your household’s wealth.

Let Compound Interest Work for You

Compound interest is your interest earning interest. While the concept may work against you when you take out a loan to buy a car or use your credit card, it works in your favor when you’re saving money. For example, if your savings is growing at a rate of four percent, your investment will double in eight years and quadruple in 16 years. Your money will grow exponentially the longer you save: the more money you’ve saved, the more your money will grow.

Tap into Your Home Appreciation

Experts expect home prices to appreciate 3.24 percent and grow by 21.4 percent cumulatively.2 If a homeowner purchases a home this year for $250,000, they could earn more than $40,000 in equity over the next five years. Although the home value of the average American family’s home is $165,000, home values vary by market.3 If you’re curious about the value of your home, give me a call!

Build Equity in Your Home

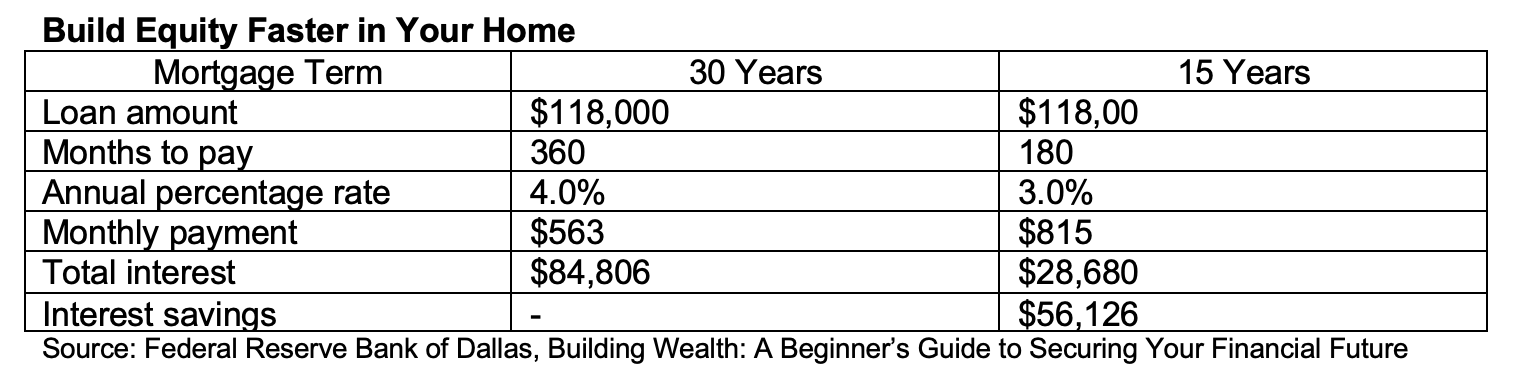

One of the most compelling reasons to own a home is it allows you to build wealth over time. According to previous studies, the average homeowner has a net worth of $200,000, which is 31 to 46 times the net worth of the average renter. Saving for a down payment, especially if you plan to put down more than 20 percent, helps you adopt good financial habits. The more you put down when you buy, the higher your share of equity when you close. Although for the first five to seven years, the majority of your payment will go toward interest, over time more money will be applied to the principal. There are many tools online that calculate your current and future equity in your home, including this one here.

Build equity sooner by choosing a shorter amortization term. While your payment may be higher, you’ll likely qualify for a lower interest rate and will pay less interest over the life of the loan.

Pay Down Your Mortgage…or Not

Many homeowners grapple with whether or not to pay down their mortgage. On one hand, if you pay it down, or pay it off early, you’ll save money on interest, which you can use to make other investments. On the other hand, if your goal is to be debt free, it’s better to pay off your higher-interest debt, such as credit card debt, first before paying down your mortgage debt. Additionally, if you’re saving for retirement, putting extra cash toward your retirement accounts will help you build a nice nest egg to enjoy later on.

If you decide to pay off your mortgage sooner, here are a few ways to do so:

- Pay more money at the beginning of your amortization period and apply it to your principal.

- If you receive a tax refund or other windfall, apply it toward your principal.

- Make one extra payment each year. You’ll save money on interest and pay your loan off sooner.

- Add an extra $50, or another amount you can afford, to the principal of your payment each month.

- If you locked into a 30-year fixed loan, refinance to a shorter, 15-year fixed loan. Your payment may be higher, but you’ll pay it off sooner.

Your financial advisor can help you decide if paying off or paying down your mortgage is right for your goals.

Purchase Investment Property

Investment properties provide passive income to your growing financial portfolio. More than 25 percent of Americans say real estate is the best way to invest money you may not need for the next 10 years. While many people flip houses to make money—that is, they buy a home at a low price, fix it up and sell it quickly—others purchase multifamily properties to create monthly cash flow to save or to reinvest in other properties.

The longer you own a property, the better investment it becomes as you’ll continue to build equity. While rental costs rise with inflation, your mortgage will remain the same. The best part? Once you pay off the mortgage, your cash flow will increase. Remember to create a budget for maintenance each month, between 10 to 20 percent of the rent you receive, or more if the home is older. This will help you save more money in the long run and allow you to prepare for unexpected repairs.

There are tax benefits to owning investment property as well. You may be able to claim deductions for depreciation, as long as it fits within the guidelines; repairs, travel expenses, interest and more. If you’re thinking of purchasing investment property, talk to your tax professional to get the details.

Achieve More Wealth by Creating Financial Goals

Setting a goal will help you achieve your desired level of wealth. Once you achieve one goal, reassess and set the bar higher.

- What is your idea of wealth? Your idea of wealth will change as you earn more money. That’s why it’s vital to set goals along the way. What do you want your net worth to be in 5 years, in 10 years and in 20 years?

- Write down your short-term and long-term goals. Once you have determined your goals, write them down. This is the first step towards getting your desires out of your mind and into motion and it will be easier to refer to them later on.

- Develop a budget to help you reach these goals. A budget not only helps you understand where your money goes each month, it may also prevent you from overspending. That way you can have more money to save and invest.

To increase the amount you can invest, make adjustments to your daily spending and monthly bills, if possible. Look for opportunities to save money and transfer that savings into your accounts.

It’s never too late to begin building your family’s wealth. Whether you’re interested in buying a first home, upgrading to a larger home or are thinking of renovating, I have you covered. Give me a call and I’ll answer all of your real estate questions and offer suggestions to help you increase the value of your home.

2022 Sources

-

- https://www.bankrate.com/personal-finance/average-net-worth-by-age/

- https://www.forbes.com/advisor/mortgages/real-estate/housing-market-predictions/

- https://traceydesimon.com/

- https://zillow.mediaroom.com/2022-06-07-Hot-housing-market-not-a-bubble,-economists-say

- https://www.onlinewbc.org/mortgage-calculators/real-estate-equity-growth-schedule-calculator.html